by Michael Beckley, The New York Times, August 19, 2024

In the 2000s, former President Hugo Chávez of Venezuela bet his country’s economic future on a rising China, securing tens of billions of dollars in investments and loans-for-oil deals. It paid off at first. China voraciously consumed Venezuelan oil and financed infrastructure projects, such as a high-speed railway and power plants.

The 2010s brought a reckoning. Oil prices fell, and growth in Chinese oil demand slowed along with its economy. Venezuela’s oil export revenues plummeted, to $22 billion in 2016 from more than $73 billion in 2011. Misrule by Mr. Chávez and his handpicked successor, Nicolás Maduro, and myriad other domestic problems already had Venezuela on the brink; the gamble on China helped push it over the edge. In 2014, Venezuela’s economy collapsed. People scavenged for food in garbage dumps, hospitals were short of essential medicines and crime surged. Since then, nearly eight million people have fled the country. China largely cut Venezuela off from new credit and loans, leaving behind a slew of unfinished projects.

Venezuela’s over-dependence on China was an early warning that the world ignored. Dozens of other countries that rode China’s rise are now at serious risk of financial distress and debt default as the Chinese economy stagnates. Yet China refuses to offer meaningful foreign debt relief and is doubling down at home on its protectionist trade practices when it should be undertaking reforms to free up and restart its economy, the world’s second-largest and a crucial engine of global growth.

That is the flip side of China’s “miracle.” After the 2008 global financial crisis, the world needed an economic savior, and China filled that role. Starting in 2008, it pumped $29 trillion into its economy over nine years — equivalent to about one-third of global G.D.P. — to keep it going. The positive ripple effects were felt worldwide: From 2008 to 2021 China accounted for more than 40 percent of global growth. Developing countries eagerly attached themselves to what seemed like an unstoppable economic juggernaut, and China became the top trading partner for most of the world’s nations. Like Venezuela, many discovered that the booming Chinese economy was a lucrative new market for their commodity exports, and they leaned heavily into that, allowing other sectors of their economies to languish.

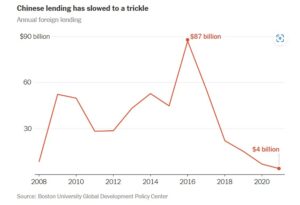

China also lent more than $1 trillion abroad, largely for infrastructure projects to be built by Chinese companies under its Belt and Road Initiative. Over the past two decades, one in three infrastructure projects in Africa was built by Chinese entities. The long-term debt risks for fragile developing economies were often ignored.

Source: Boston University Global Development Policy Center

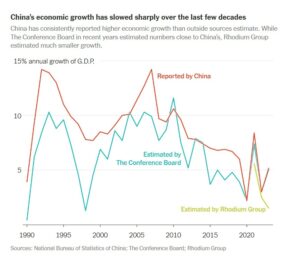

Sources: National Bureau of Statistics of China; The Conference Board; Rhodium Group

Note: Trade data as of 2023. For countries where 2023 data is not available, the most recent year is used. Trade figures are reported annually from each nation and may still be incomplete.

Zambia and Sri Lanka defaulted on billions in debt owed to international creditors in 2020 and 2022, respectively. In both cases, an explosion of Chinese loans and credit was a significant factor in pushing those countries into deep financial trouble. This led to debt restructuring negotiations that were difficult and protracted partly because of the opaque nature of Chinese lending practices, exacerbating both countries’ crises. Eventually, Zambia and Sri Lanka were forced to extend repayment periods, so resources that could have been spent on economic recovery went to servicing debt obligations. The extended uncertainty has made it difficult for these countries to acquire new financing.

The International Monetary Fund and the World Bank have warned that dozens of countries across the developing world — many of which have close trade relationships with China — now face some form of debt distress. Pakistan is mired in a deep economic crisis that it can’t climb out of, partly because of the need to pay back billions of dollars in loans to China for infrastructure and other projects. Some factories in the country have been idled because they have been unable to buy necessary materials and because the government can’t afford to maintain a stable power supply. In Laos, around half of the nation’s foreign debt is owed to China, which extended billions of dollars in loans for projects including a China-Laos high-speed rail line that has been widely panned as a white elephant. The heavy debt has hammered Laos’s currency, making it more difficult for the country to service its debt and forcing it to cede some of its economic sovereignty as repayment, including allowing China to take ownership stakes in its power grid.

Even some wealthy nations such as Germany, the economic powerhouse of Europe, face deep challenges because of their over-dependence on doing business with China. German exports to China fell 9 percent last year — the steepest decline since China joined the World Trade Organization in 2001 — and Germany’s economy shrank that year, too. Major commodity exporters such as Australia, Brazil and Saudi Arabia are vulnerable since exports of energy, metals or agricultural products to China make up significant portions of their economies.

There are worrying parallels between today’s situation and the debt crisis that swept through developing countries in the 1980s. Many nations, particularly in Latin America and Africa, were burdened with massive debts primarily owed to Western commercial banks and international institutions such as the I.M.F. and the World Bank. Facing soaring interest rates and plummeting commodity prices, nations including Mexico, Brazil and Argentina defaulted. Some endured years of subsequent low economic growth, severe austerity measures, plummeting living standards and political upheaval.

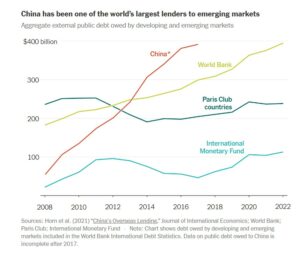

China, now by far the world’s largest sovereign lender, has played a leading role in saddling many countries with levels of debt, often through nontransparent arrangements, that are comparable with those seen in the 1980s. The situation is becoming perilous. Over the past decade, during which China doled out more lending than the Paris Club — a grouping of 22 of the world’s largest creditor nations — the total value of interest payments of the 75 poorest countries in the world have quadrupled and will outstrip their total annual spending on health, education and infrastructure combined, according to the World Bank. An estimated 3.3 billion people live in countries where interest payments exceed investments in either education or health, the United Nations said.

Sources: Horn et al. (2021) “China’s Overseas Lending,” Journal of International Economics; World Bank; Paris Club; International Monetary Fund

Note: Chart shows debt owed by developing and emerging markets included in the World Bank International Debt Statistics. Data on public debt owed to China is incomplete after 2017.

Such steps will have only a limited impact unless China is confronted over its role in exacerbating these problems and failing to address them. Finding the collective international resolve needed to get China to change its self-serving ways will be difficult. The crucial first step is to recognize the scale of the problem.